10 Mint Alternatives to Make Budgeting Easier

Some products in this article are from our partners. Read our Advertiser Discloser.

Looking for an alternative to Mint? Mint is a great product, but unfortunately, it shut down in March of 2024.

Check out this list of the best Mint alternatives to see if you might find a money app for you.

Top Alternatives To Mint

Finding the right budgeting tool is important. Here’s a little bit about how each Mint alternative works so you can decide for yourself.

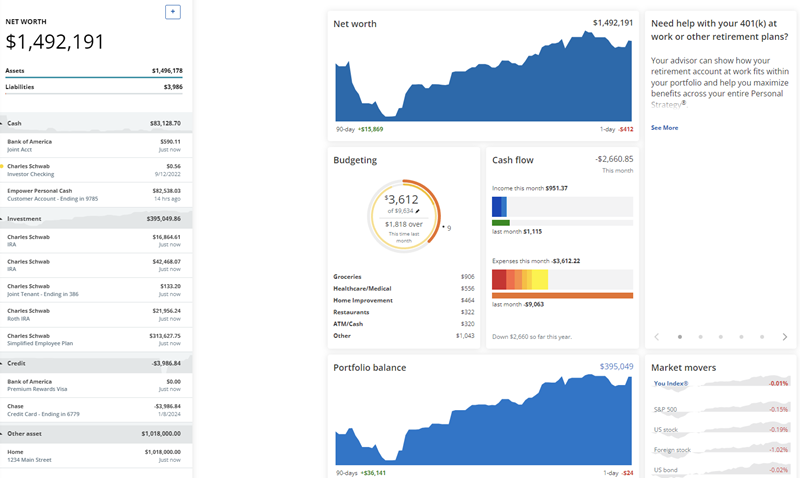

1. Empower

Empower is one of the best Mint alternatives. This is because it is a free app that you can link your financial accounts and see your entire financial picture in one place.

The Empower dashboard will show you information such as:

- Your net worth

- Portfolio balance

- Retirement savings for the year

- Spending information by category

- Bill payment due date notifications

- Whether you’re on track with your designated budget

Empower offers many of the same features as Mint but with more emphasis on investments. Both Mint and Empower have great tracking and budgeting tools.

Read our full Empower review.

2. Tiller Money

Tiller Money is an alternative to Mint that helps you manage your money using spreadsheets. It works with both Excel and Google spreadsheets.

Tiller starts you off by having you sync up your bank, loan, and other accounts. Then, it lets you create customized spreadsheets to begin tracking and budgeting.

It has a variety of spreadsheet templates:

- Monthly budget spreadsheet

- Net worth tracker

- Weekly expense tracker

- Debt snowball spreadsheet

And others. In addition, you can create your own custom spreadsheets if you choose. The interface is very easy to use. The platform costs $79 a year.

Read our Tiller Money review.

3. You Need a Budget (YNAB)

You Need a Budget (YNAB for short) is a budgeting tool that helps you gain total control of your money.

They created the YNAB budgeting plan, which consists of four basic rules:

- Give every dollar a job

- Embrace your true expenses

- Roll with the punches

- Age your money

YNAB states that the average new user will save $200 in the first month alone. YNAB can help you create your budget, track your spending, create and track goals, form a debt payoff plan and more.

Both Mint and YNAB do a fabulous job helping you with your budget. But the main difference between the two is the cost. YNAB is $84 per year. Mint is free. Note that students do get YNAB free for the first year.

And YNAB has a free 34-day trial to try it out at no cost.

Read our full YNAB review.

4. EveryDollar

EveryDollar is a budgeting tool created by popular personal finance expert Dave Ramsey. It helps you manage your money on the premise of a zero-sum budget.

It doesn’t offer much for features besides budgeting, but the program is easy to use. In addition, it shares Ramsey’s baby steps in case you want to take your finances to a higher level.

EveryDollar’s free version requires you to enter your transactions manually. However, you can purchase another version: EveryDollar Plus.

The Plus version will sync your transactions up automatically, but it costs $99 per year ($8.25 per month).

Read our full EveryDollar review.

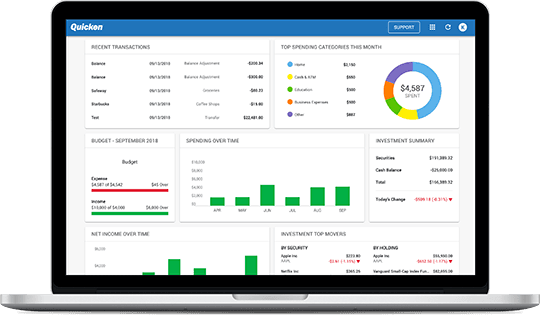

5. Quicken

Quicken is one of the most well-known alternatives to Mint. It was the pioneer budgeting tool.

Quicken has four plans available ranging from $34.99 – 89.99 per year. Both Quicken and Mint allow you to import your transactions automatically.

In addition, both allow you to monitor your credit score and send weekly email summaries.

Related Article: 15 Best Quicken Alternatives

6. CountAbout

CountAbout is an app with automatic transaction syncing and customizable income and spending categories and tags.

One neat feature about CountAbout is that it’s the only budgeting tool that allows you to import data from Quicken and Mint. This is a great feature if you’re interested in making a switch.

CountAbout has two versions: the basic version, which is $9.99 per year, and the premium version, which is $39.99 per year.

7. PocketSmith

PocketSmith was founded by a group of people from New Zealand.

They have three plans you can choose from:

- A basic plan that’s free and requires manual imports of transactions

- A premium plan that costs $9.95 a month and imports transactions automatically for ten accounts

- A “super” plan that costs $19.95 a month and allows you to add unlimited accounts

The app also has a “projection” feature that allows you to see six months or more into the future. It shows you your financial future based on your current income and spending.

The free plan gives you a six-month projection. The Premium plan gives you a 10-year projection. And the Super plan gives you a 30-year projection. This can be a nice feature.

8. Status Money

Status Money is one of the newer apps as an alternative to Mint, with many of Mint’s features. It allows you to track your money by auto-syncing your bank accounts. And like Mint, Status Money is free.

One added benefit of Status Money is that it allows you to see how other members are saving and spending. The site gives you charts that compare your savings and spending numbers to those of your peers.

You can use the peer group that Status Money creates for you, but you can also create your own peer group and share numbers with your friends.

This can make for some fun motivation to improve your money situation.

9. Qube Money

We love Qube Money because they offer a digital envelope system. Yes, a digital envelope system that helps you stay on budget.

Qube is easy to use. After you open an account, you deposit money from your main bank account into your Qube account.

You can also set up Direct Deposit from your employer into Qube as opposed to your regular bank account.

Qube is FDIC-insured and allows you to get direct deposit two days earlier.

You then create individual Qubes (envelopes) to allocate the money. Every dollar has an assignment. Therefore, there is no room for unplanned spending.

Related Article: Qube Money Review

10. Copilot

Copilot is one of the newest budgeting apps. In fact, you can import your Mint app data right to Copilot.

Based on our research, most users felt the data after downloading was pretty accurate regarding categories.

One of the features we like is that the app can track your recurring transactions. This means it helps you plan your budget by knowing where the money is going and what is left to help you plan ahead.

For example, if you have a school payment and mortgage due on the 1st, you can see what is available for your electric bill. Which obviously will fluctuate throughout the seasons.

With a 4.8 Star rating out of 5 stars with over 8K reviews on the Apple Store, most users felt the $70 annual cost was manageable.

Mint Alternative Comparison Table

| Company | Trustpilot |

| Empower | 3.8 |

| Tiller Money | 3.5 |

| You Need a Budget | 3.8 |

| EveryDollar | 3.6 |

| Quicken | 3.6 |

| Status Money | N/A |

| Countabout | N/A |

| Pocketsmith | 2.9 |

| Qube Money | N/A |

| Copilot | N/A |

Summary

Mint has some terrific budgeting features for users at no cost to you. However, there are many other budgeting options out there.

Depending on your preferences and your budget, you might find a Mint alternative that is better for you. However, if you’re looking for basic and free, Mint should cover you just fine.

Its main competition is Empower, which offers a lot more features for the same amount of money: FREE.